🌿 Landscaping Insurance Coverage Calculator

Estimate the right coverage levels for your landscaping business based on crew size, equipment & services

| Policy Type | Who Needs It | Typical Coverage | Notes |

|---|---|---|---|

| General Liability | All landscapers | $1M – $5M per occurrence | Covers property damage & bodily injury |

| Workers Compensation | Any with employees | State-mandated amounts | Required in most states with 1+ employees |

| Commercial Auto | Company vehicles | $300K – $1M combined | Personal auto does not cover work use |

| Tools & Equipment | Equipment owners | Replacement value | Covers theft, damage on/off site |

| Pollution Liability | Chemical applicators | $1M – $2M | Required for pesticide/herbicide work |

| Commercial Umbrella | Medium/large operations | $1M – $5M excess | Sits above GL and auto policies |

| Inland Marine | Mobile equipment users | Per equipment value | Covers equipment in transit |

| Professional Liability (E&O) | Design businesses | $500K – $2M | Covers design errors & omissions |

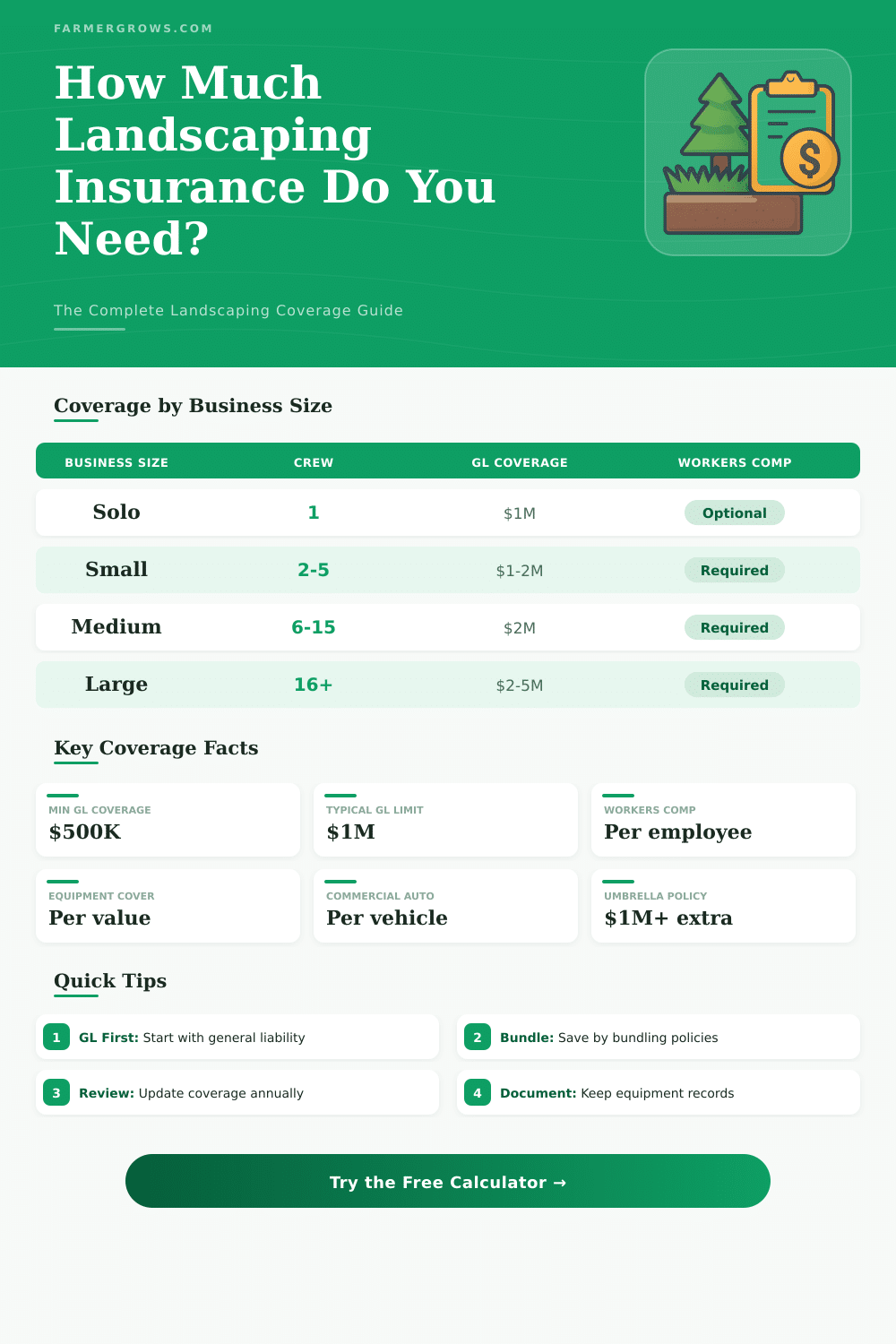

| Business Size | Employees | Recommended GL | Workers Comp | Umbrella |

|---|---|---|---|---|

| Solo Operator | 1 (owner only) | $500K – $1M | Optional / self | Optional |

| Micro Business | 2 – 4 | $1M | Required | Recommended |

| Small Company | 5 – 10 | $1M – $2M | Required | Recommended |

| Medium Company | 11 – 25 | $2M | Required | Required |

| Large Company | 26 – 50 | $2M – $3M | Required | Required |

| Enterprise | 51+ | $3M – $5M+ | Required | Required |

| Service Type | NCCI Class Code | Risk Level | Notes |

|---|---|---|---|

| Lawn & Garden Maintenance | 0042 | Medium | Most common landscaping code |

| Tree Pruning / Trimming | 0106 | High | Higher rate due to fall risk |

| Tree Removal / Felling | 0106 | Very High | Highest risk classification |

| Snow Removal | 9014 | Medium-High | Seasonal, slip/fall risks |

| Irrigation Installation | 6217 | Medium | Plumbing-adjacent work |

| Hardscape / Pavers | 5221 | Medium-High | Heavy materials, machinery |

| Chemical Application | 0042 + endorsement | High | Requires pollution liability add-on |

| Risk Factor | Coverage Impact | Additional Policy Needed |

|---|---|---|

| Chemical / Pesticide Use | +15% – +25% to GL | Pollution Liability required |

| Tree Climbing / Removal | +20% – +40% to WC | Separate high-risk WC code |

| Snow & Ice Operations | +10% – +20% to GL | Snow removal endorsement |

| Subcontractors Used | +10% – +15% | Additional insured endorsement |

| Commercial Clients | +5% – +15% | Higher GL limits required |

| Equipment > $50K | Proportional to value | Inland marine / floater policy |

| Night / Weekend Work | +5% – +10% | No extra policy, higher limits |

Landscaping insurance cost must be part of the budget for every business that involves itself about gardening or lawn care. Basic policies commonly cost less than one hopes… Some start at only 31 dollars per month, what matches around 336 dollars yearly.

Even so, the price can rise according to the kind of services, that one offers, the place of the business, the number of employees and many other factors. The most common starting points move a bit more upward near 50 dollars monthly.

How Much Does Landscaping Insurance Cost and Why

Across the United States, landscapers pay on average around 52 dollars monthly for coverage. But the reality one sees clearly, when one compares different kinds of services. Professional lawn care workers can pay around 46 dollars monthly, while those that handle tree removal commonly face 138 dollars.

Such differences have their logic, jobs with bigger risk simply require higher insurance.

General liability insurance offers quite a broad range for landscapers. The most common policies fall between 500 and 2 300 dollars per year, although more full calculations raise the annual Landscaping insurance cost to 1 100 to 3 500 dollars. For a typical company about landscape design, general liability policies costs around 51 dollars monthly.

Limits of coverage usually reach one million dollars for one event with two millions for the whole period. That same model, one million per event and two millions for total; is what the most common lawn care businesses ultimately chose.

Location affects more strongly, than one thinks. In California, the price reaches clearly higher 135 dollars monthly compared to the national average of 121 dollars. New York stays in a similar range, around 140 dollars.

Policies for business owners follow the same path in those states, where they cost much more.

Some insurance providers offer creative and flexible solutions. One can adapt the coverage according too the work, per month or per whole year. Insurance according to need does itself popular, because it allows owners to choose coverage per hour, day, week or month, especially helpful, when the work adjusts according to seasons.

At some companies, insurance for lawn care ranges from 8 dollars per hour to around 43 dollars monthly. One particular plan through a partner of Progressive reaches 650 dollars yearly.

What truly determines the price? Limits of coverage are the main cause, stronger protection wants bigger payments. Added employees raise the cost, especially when enters compensation for workers.

The services themselves play a big role. A solo contractor, that simply mows, pays less than a big team, that involves itself in tree removal and full gardening. Past history, the whole size of the business and use of subcontractors all affect it.

Some insurance premiums tie directly to the income of sales, so in a more successful business, the higher becomes the price.

What truly is protected? General liability helps in cases like a client, that falls over gear, damage to property during work or injury to anyone because of an accident. Insurance for gear helps businesses recover quickly after a loss, what cuts toll of time and not received incomes.

Commercial vehicles add extra weight to the total expense. Working with a local agent for commercial insurance commonly counts (they can get offers), thatcovers liability, gear, labor compensation and everything else, what answers for the particular business.